Will consumer confidence bring back the housing market?

The Fed met January 30th through 31st and decided to keep its benchmark rate at a range of 5.25% to 5.50%, which it’s held since July 2023. We now expect rate cuts to begin closer to summer rather than in spring. Fed chairman Powell’s rationale is reasonable: the current rate levels seem to be working, and if it’s not broken, don’t fix it. The Fed’s dual mandate is for stable prices (inflation ~2%) and low unemployment. Currently, inflation is dropping, and unemployment is low, at 3.7%. Recession fears have declined, and the soft landing — slowing the economy without recession — that the Fed intended seems to be unfolding. Powell was quick to say the Fed does not have a growth mandate, which is correct, so the risks of cutting rates early will likely outweigh the benefits of cutting in March. However, if inflation continues to fall, and economic indicators are still favorable, rate cuts will likely start mid-year.

Mortgage rates remained steady at around 6.5% in January 2024, which is still about 1% higher than needed to get more participants to enter the housing market. Sales have reached a historic low, the number of new listings coming to market are near all-time lows, and inventory has declined. This is due, in part, to normal seasonal trends — winter is when all those metrics tend to reach a seasonal bottom — but seasonality doesn’t fully explain those drops in the context of a substantial decline in rates. From October 2023 to January 2024, the monthly cost of financing a median priced home decreased nearly 13%, and the market still slowed on both the buyer and seller sides of the market, implying that rates are still too high for most would-be participants. However, we believe that if rates fall another percentage point, which roughly equates to another 10% decrease in monthly financing costs, the market will react positively and price more people into the housing market.

Another important aspect of the current market is the very recent positive changes in workers’ real earnings. The psychological effects of nearly 10 years of earnings growth, culminating in a final jump in the first two quarters of 2020, before dropping rapidly once COVID hit and inflation rose, was perhaps the most significant cause of the low economic sentiment in 2022 and most of 2023. People quickly become attached to the amount of money they make and the spending power of that money. It’s also fair to say that part of the American dream is progressively increasing earnings as we age. From 2021 to 2023, the purchasing power of the U.S. dollar declined 15%; therefore, earnings needed to increase 15% just to feel as financially well off as three years prior. For many, if not most people, earnings weren’t keeping up with inflation, and people don’t tend to buy homes when they feel less wealthy. However, after six straight quarters of real earnings growth, it makes sense that people broadly feel better about their finances, which will benefit the housing market.

The Local Lowdown

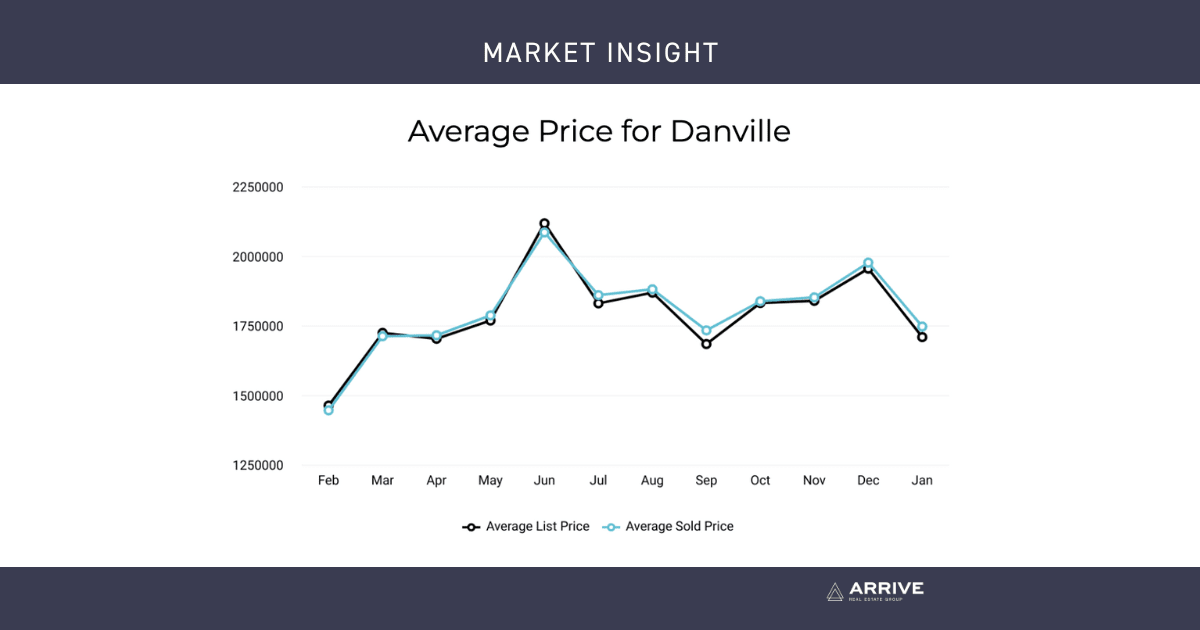

In the East Bay, low inventory has more than offset the downward price pressure from higher mortgage rates, and prices generally haven’t experienced larger price drops from higher mortgage rates. Month over month, in January, the median single-family home price fell 5% in Alameda and 4% in Contra Costa. However, year over year, prices were up 9% in Alameda and 6% in Contra Costa. We expect prices in the East Bay to remain below peak in the winter months, but as interest rates decline, prices could stretch near highs in 2024.

High mortgage rates soften both supply and demand, so ideally, as rates fall, far more sellers will come to the market. Rising demand can only do so much for the market if there isn’t supply to meet it. Unlike 2023 inventory, 2024 inventory has a much better chance of following more typical seasonal patterns. In January new listings rose 141% month over month, and homes coming under contract increased 20% but the East Bay market still favors single-family homes. Sellers also received an additional 4% of list price when compared to January 2023, a trend we expect will continue.

As always, Arrive Real Estate Group remains committed to helping our clients achieve their current and future real estate goals. Our team of experienced professionals are happy to discuss the information we’ve shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home.