If you’re an avid reader of our newsletters, you may recall discussions of a possible recession a few months ago. We, of course, weren’t the only ones talking about it, but it was a little early to opine. We’re happy to say that a recession likely isn’t on the horizon but rather that we’re entering a period of slower economic growth.

Recessions used to be defined by a fall in Gross Domestic Product (GDP) for two consecutive quarters. For what it’s worth, Real GDP in the fourth quarter of 2022 was up 1% year-over-year and 0.7% quarter-over-quarter. However, the National Bureau of Economic Research (NBER) takes a more nuanced approach by considering nonfarm payrolls, industrial production, and retail sales, among other indicators. The U.S. employment rate is still strong despite some notable high-profile companies, especially in tech, announcing mass layoffs. The unemployment rate is 3.5%, which is about as low as we’ve seen in modern history. Additionally, initial unemployment claims and continued claims have been at pre-pandemic levels for about 13 months and 11 months, respectively. Total Nonfarm Private Payroll Employment data (seasonally adjusted) from ADP shows that job growth stagnated in the second half of 2022 but didn’t decline. With over 10 million job openings in the country, the level of unemployment should remain historically low for the foreseeable future.

Inflation is still far above the Fed’s 2% target, but it is coming down. December 2020 was the last month of the steady ~2% year-over-year inflation rate we’d seen over the past decade. Inflation rose rapidly in 2021 and the first half of 2022. Early signs show we are entering a period of disinflation where goods and services will get more expensive at a slower rate than we’ve seen over the past two years. We expect mortgage rates to hover around 6% for the first half of 2023 as they are typically about 1.8% higher than 10-year U.S. Treasury bond yields. There is potential for rates to come down slightly this summer.

Local Lowdown

We can expect low inventory will remain the norm for at least six months, if not the next year. The housing market hasn’t come to a grinding halt — people will always need to move for an assortment of reasons — but it has slowed considerably, largely due to financing costs and the aftermath of the buying frenzy from mid-2020 to mid-2022. The 2020-2022 housing market was very efficient compared to now. Real property tends to be much further toward the inefficient side of the spectrum for a slew of reasons: the unique nature of every home, finite amount of land, building expense, number of market participants at any given time, high cost, long holding period, and opaque pricing, which creates a relatively illiquid market.

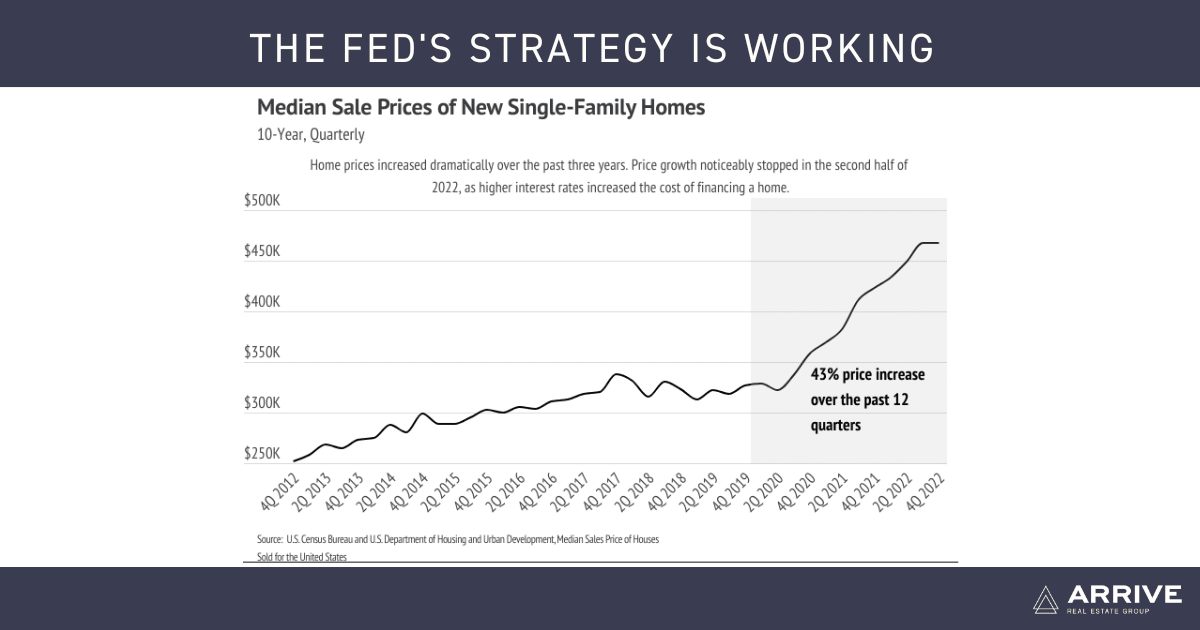

Even with the large contraction in the second half of 2022, when we account for price increases and rate increases, the price of a home has increased 82% over the past three years. Every market has had different levels of price appreciation and contraction in the recent past, but everyone currently faces higher mortgage rates. It’s reasonable to assume that the market will slow after such a dramatic increase in cost.

Alameda inventory fell to an all-time-low in January 2023, while the number of homes for sale in Contra Costa landed slightly above the record low reached in December 2021. Higher interest rates have dropped incentives for potential sellers and buyers while homeowners who either bought or refinanced recently locked in a historically low rate, so fewer listings are coming to market. Many potential buyers were priced out of the market as interest rates rose. New listings fell by 29% year-over-year, while sales declined by 41%. In the East Bay, inventory moved slightly higher in January, but still all indications are that we are still in a sellers’ market.

As always, Arrive Real Estate Group remains committed to helping our clients achieve their current and future real estate goals. Our team of experienced professionals are happy to discuss the information we’ve shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home.