March Market Update: Historical Review and East Bay Market

Real Estate

Real Estate

We don’t want to jinx anything, but we may have turned the corner on the pandemic! New cases are declining after peaking in early January, and the United States is administering more vaccinations every day. However, COVID-19 will have lasting effects on how we live and work. Working from home is here to stay, and all-time-low mortgage rates have incentivized renters to enter the housing market because the cost of buying may be lower than renting. For these reasons, we suspect that demand will continue to remain high through 2021.

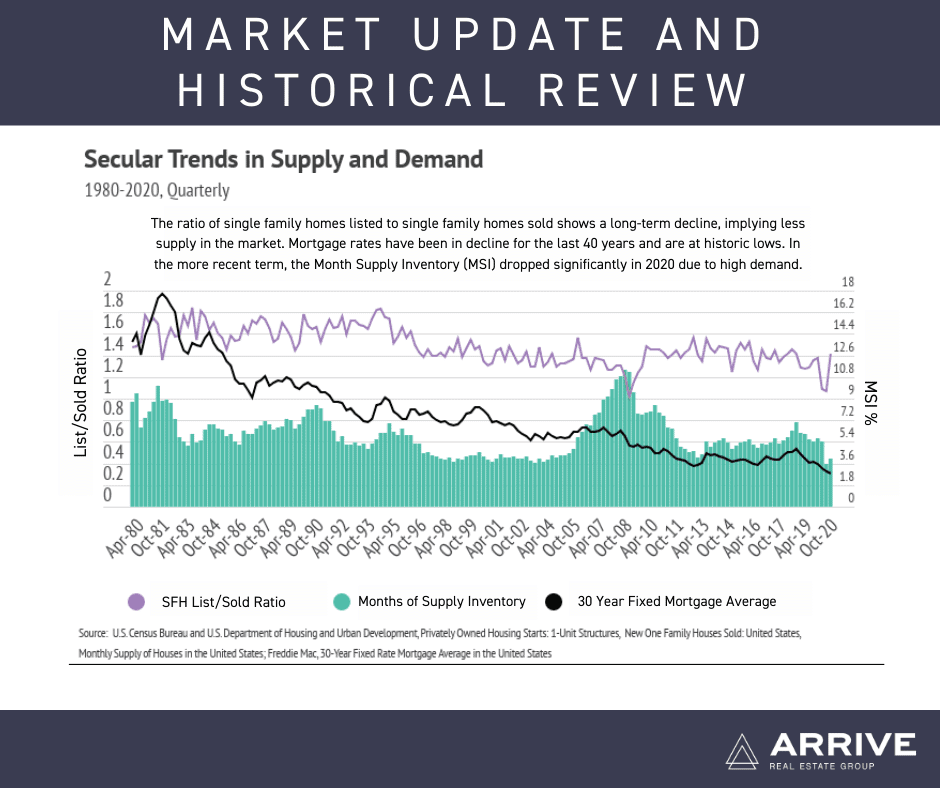

In our March market update, we will analyze at secular trends (trends that are neither seasonal nor cyclical) to help us understand the current housing environment. Let’s look at levels of supply and demand, Months of Supply Inventory (MSI) and mortgage rates over the last 30 years.

The early 1980s marked the highest mortgage rates in the United States—over 18%—as well as the secular decline in rates since that peak. During the 16-year period between 1980 and 1995, the ratio of houses listed to homes sold stayed fairly stable, which is ideal in terms of equilibrium in supply and demand. However, MSI began to shift lower around 1990, indicating that demand was increasing relative to supply. We saw a small peak in MSI in 1995, which declined until the housing bubble began to burst in 2005. During this period, mortgage rates experienced the steepest drop, with an approximately 11% decline. The difference in mortgage payment from 18% to 7% equates to about $10,000 per month in savings on a $1 million mortgage, making homes much more affordable.

This period contained an economic growth cycle. Demand for housing dramatically increased, while the ratio of houses listed to homes sold declined and MSI decreased and held at around four months of supply. Credit lending standards during this 11-year period were extremely lax while mortgage rates continued to decline, which further increased demand. Home prices more than doubled from 2000 to 2005. This period marked the beginning of the housing market decline and home appreciation deceleration.

Typically, MSI and the ratio of houses listed to homes sold track together, but from 2005 to 2010, they started to show an inverse relationship. MSI rose, while the ratio declined. This happened because, with the Great Recession, demand and new production dropped precipitously and didn’t rebound until 2012. After 2012, the housing recovery began, and we experienced another stable state with fairly steady supply and demand dynamics and consistently low mortgage rates.

During the pandemic and the resulting recession in 2020, mortgage rates fell further, and demand increased dramatically. MSI dropped sharply in 2020 due to high demand and dwindling supply. Mortgage rates have never been lower, which incentivizes more people to enter the market.

It’s difficult to overstate just how unique homebuying trends were in 2020. The homeownership rate increased 2.6% over a single quarter. For reference, out of 223 quarters, only three other quarters had a change above 1%. This was a gigantic jump.

Although we do not expect the same level of buying in 2021, the environment is right for sustained high demand. Supply remains low, and we anticipate a competitive landscape for buyers over the course of this year.

The median single-family home price rose to another all-time high, and year-over-year, single-family home prices increased considerably, up 20%.

Single-family home inventory remained lower through 2020 relative to 2019, which speaks to the desirability of the East Bay area. During the pandemic, fewer people wanted to leave, and more people wanted to move to the area. New listings throughout the year were lower than normal, while sales were much higher. By the end of 2020, sales remained steady as new listings declined. With such a consistent level of demand, prices will likely continue to appreciate throughout 2021.

Days on Market (DOM) declined further for single-family homes throughout 2020, but spent less time on the market in December 2020 than they did in December 2019. This allowed the Month Supply Inventory (MSI) to drop further in December 2020 to 0.4 months which firmly favors sellers.

In summary, the high demand present in the East Bay has buoyed home prices. The housing market has shown its resilience through the pandemic and remains one of the most valuable asset classes.

We anticipate new listings to increase around March 2021. While the winter season tends to see a slowdown in activity, December 2020 showed higher-than-normal sales despite lower-than-normal inventory, once again highlighting the desirability of East Bay.

As always, Arrive Real Estate Group remains committed to helping our clients achieve their current and future real estate goals. Our team of experienced professionals are happy to discuss the information we’ve shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home.

Stay up to date on the latest real estate trends.

You’ve got questions and we can’t wait to answer them.