The average 30-year mortgage rate hit a 23-year high in September, closing the month at 7.31%. The current high mortgage rates are negatively affecting affordability, making it incredibly hard not to compare mortgage rates and prices to those of the past few years. Only 27% of homes were purchased with cash in August, a good portion of which were likely bought by homeowners selling their home and using the proceeds to buy another. Most buyers, however, are financing the purchase of their homes in some capacity and are, therefore, affected by the high mortgage rates. The median home financed in August 2023 cost 15% more on a monthly basis than the median home financed in June 2022 — the all-time high price — because rates are 1.8% higher.

As you’ve likely already noticed, our current market involves an interesting dynamic of low supply and demand, but high prices and cost of financing. A lot of this has to do with (potential) seller mentality. Approximately 75% of U.S. homeowners have mortgage rates of less than 4%, according to JPMorgan, which has kept potential sellers from entering the market because they either stay in their home or keep their home as a rental property when they move. As a result, new listings remain significantly depressed. When we compare the first three quarters of 2022 and 2023 with the average from the first three quarters of 2017 to 2021, new listings are below average by about 1.5 million homes. The National Association of Realtors reported that the number of homes sold dropped 0.74% month over month and 15.3% year over year, which is less surprising considering that there are far fewer homes from which to choose. That being said, people move for all sorts of reasons, and supply has declined further than demand, which has helped prices stay high. Homebuilders are also affected by higher rates when it comes to construction loans, so homebuilder sentiment is in decline, according to the National Association of Home Builders/Wells Fargo Housing Market Index. We will likely see fewer and fewer new homes built until rates come down, negatively affecting supply.

The Local Lowdown

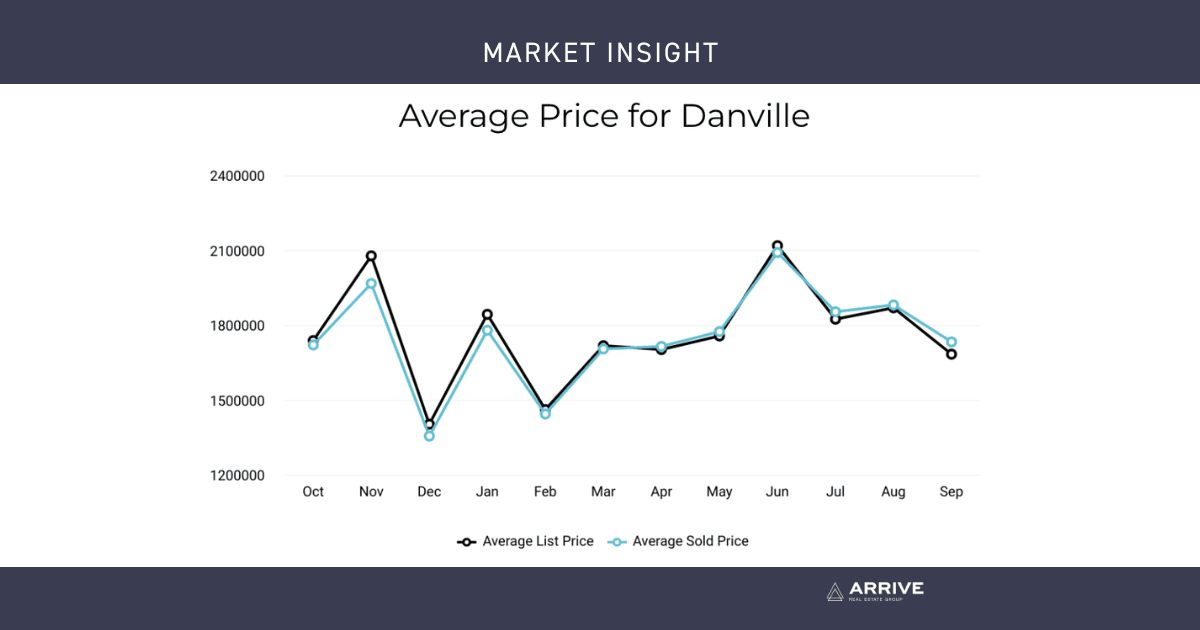

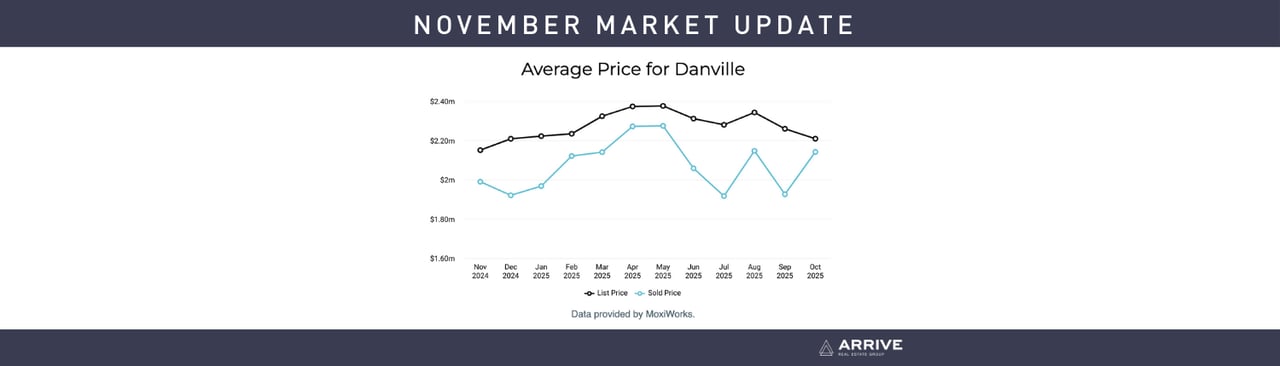

In the East Bay, the price of housing has remained sticky and has even risen during a period of rapidly rising mortgage rates. Increasing demand and low, but rising inventory helped drive the rapid home price appreciation that the East Bay experienced in the first half of the year. Single-family home prices contracted in July and August but rose in September. Year-to-date prices rose significantly across the East Bay counties. Notably, single-family home prices rose 24% in Alameda and 15% in Contra Costa this year. In the fourth quarter, we expect prices to remain fairly stable.

Typically, demand begins to decline in the fall and bottoms out in January, so the low supply of homes should be less of an issue. With mortgage rates at a 23-year high, quality listings are going to have the most competition. Potential homebuyers aren’t nearly as willing to pay a premium for a fixer upper as they were in 2020 and 2021.

Single-family home inventory has trended higher into the fall of 2023, which is far from the seasonal norm. Typically, inventory peaks in July or August and declines through December or January. Even though inventory has increased, it’s still historically low, moving higher primarily due to softening demand (fewer sales) caused by higher interest rates and normal seasonality. Overall, new listings have been exceptionally low this year. The number of home sales is, in part, a function of the number of active listings and new listings coming to market. Comparing new listings from January through September 2023 to the same time period in 2022, new listings are down 32%, which has directly impacted both inventory and sales. Sales are down 24% year over year.

Even as demand slows, sellers are maintaining more negotiating power and receiving more than asking price on average. The average seller received 95% of list in January, which grew to 104% by May. From May to September, the average seller received 104% of list in every month. That being said, the percentage of list price received tends to decline in the winter when fewer buyers are in the market. The market is still very much indicating we are in a Sellers market.

As always, Arrive Real Estate Group remains committed to helping our clients achieve their current and future real estate goals. Our team of experienced professionals are happy to discuss the information we’ve shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home.