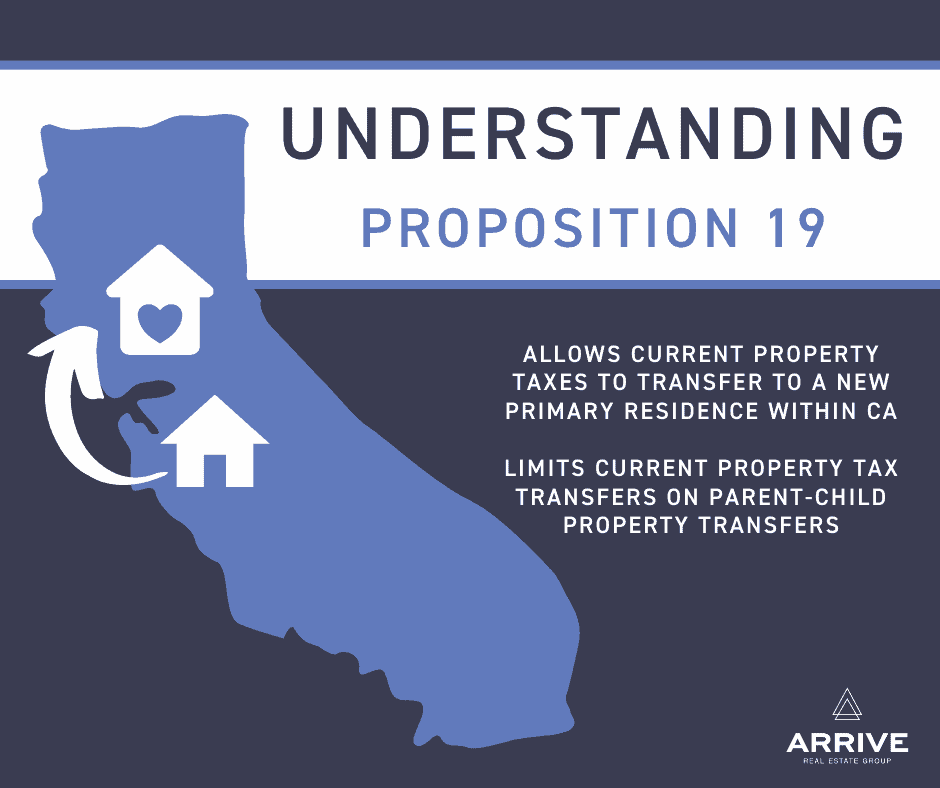

Understanding Proposition 19

Real Estate

Real Estate

In November 2020, Californians approved Proposition 19 which will make important changes to the property tax transfer rules for those aged 55 and over as well as parent-child property transfers of primary residences and parent-child transfers of other real property. The new guidelines have now replaced the existing rules of Proposition 13.

We recently held a webinar with John K. Bishop of Bishop Tax and Trust Law to explain these changes. Below is a summary of our discussion of the tax implications of Proposition 19, but please keep in mind that this is considered to be a general overview. We recommend you consult a professional to analyze your specific situation. The complete webinar can be viewed here.

Now let’s take a look at each one of these elements a little closer.

Californias are able to transfer their property tax base from their principal residence to the purchase of a replacement residence within 2 years of the sale of the existing residence, if they are over the age of 55, disabled or are able to claim disaster relief from wildfire damage. No longer does the existing and replacement property have to reside in one of the previously approved 10 counties. The residences may be in any location in California.

The value of the replacement residence can be of any value. If the value of the new home exceeds the value of the existing residence, the portion over 100% will be added to the previous tax base. Californians may use this rule up to 3 times in their lifetime, previously you were only allowed to transfer your tax base once.

As an example, Tom, age 70, wants to sell his Pleasanton home and move to San Diego. His current assessed value is $350,000 and his Pleasanton home is worth $1,500,000. His replacement San Diego home is worth $1,400,000. If Tom sells Pleasanton home and purchases the San Diego home within 2 years of sale, both after April 1, 2021, Tom will pay property tax on his San Diego home at $350,000 of assessed value, plus the 2% annual increases.

Parents are now only able to transfer a residence to their children if the property is the principal residence of the parent and the child. This also applies for children transferring a property to their parents. The new tax base of the property will be whichever is greater, the current assessed value or the market value, minus $1,000,000.

As an example, Jerry wants to leave his Pleasanton home to his son Benjamin upon his death. The home is worth $1,600,000 and Jerry’s current assessed value is $500,000. On Jerry’s death (sometime after February 15, 2021), Benjamin inherits the home. Under Prop 19, Benjamin’s assessed value will be $600,000 (greater of $1.6m less $1m and $500k), assuming that Benjamin moves into the home within 1 year of Jerry’s death.

Previously, parent-child transfers were allowed on other real property, such as a vacation home or rental property, up to $1m of assessed value without reassessment. However, this is no longer be allowed as only primary residences qualify. Any parent-child transfers of other real property will now be reassessed at the current market value.

There are a number of questions that are not yet answered by Prop 19. The CA Board of Equalization expects some additional guidance on these ambiguities. Without the additional guidance, each county may interpret the ambiguities on their own. It is important to check with the county assessor when considering a transaction to make sure they interpret it the same as you.

If you would like more to view the full webinar, request more information or have specific questions related to Proposition 19, please contact Arrive Real Estate Group.

——-

Stay up to date on the latest real estate trends.

You’ve got questions and we can’t wait to answer them.